CERM Sandbox

Enhancing financial resilience in the face of climate change

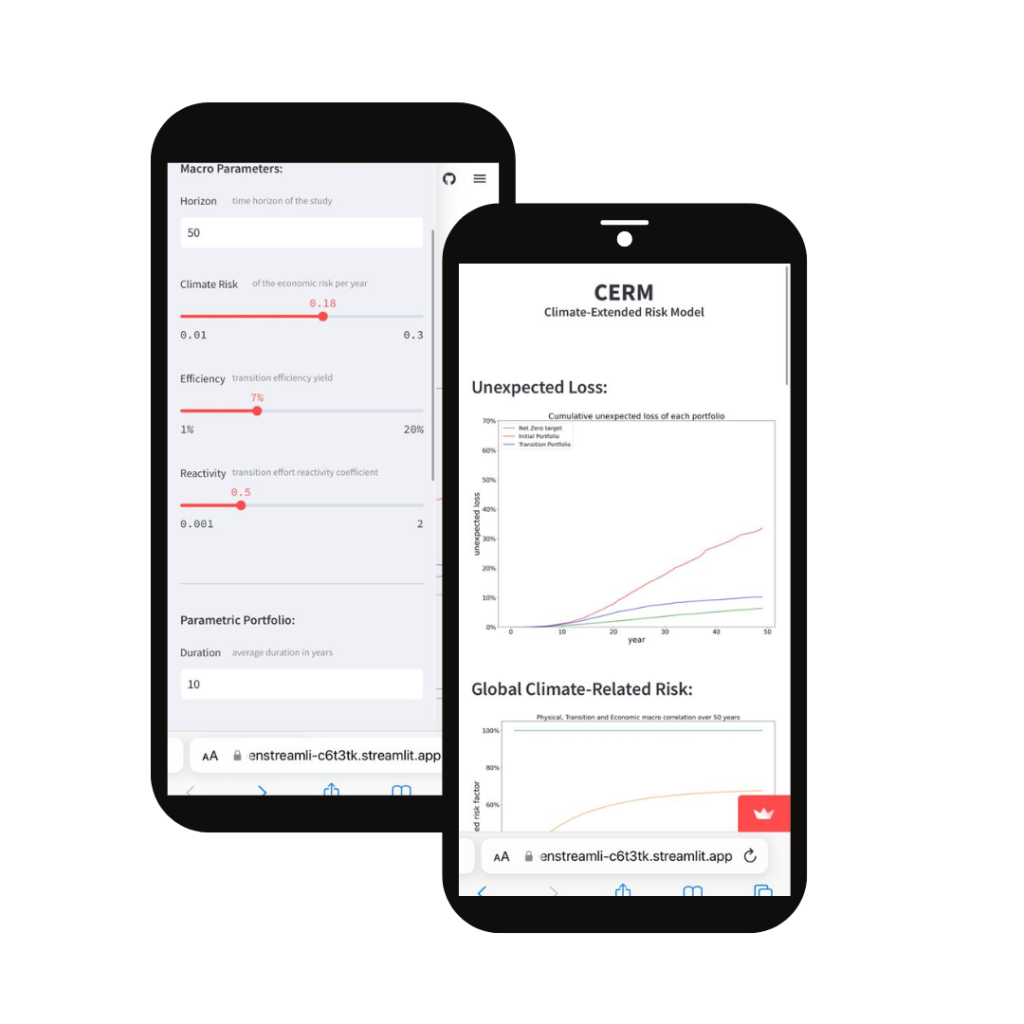

The Climate-Extended Risk Model (CERM) is a risk framework designed to enhance the resilience of financial institutions in the face of climate change. It aims to integrate emerging climate risks into the existing regulatory framework by extending the current unexpected loss credit risk model used by banks for the lending portfolio. The CERM recognizes that climate risk is a long-term, global, and evolving factor that must be considered as a systematic risk.

In the standard regulatory credit risk portfolio model, the macroeconomic cycle is the only systematic risk factor considered. Each borrower’s correlation to this macroeconomic risk is determined by its credit rating with a formula defined by the regulator, and the model assumes short-term independence of risks. However, climate risk differs from economic risk as it follows a long-term dynamic due to the accumulation of greenhouse gas in the atmosphere. It cannot be mathematically equated with economic risk and therefore needs to be modeled separately as an additional risk factor with a forward-looking and evolving distribution.

The CERM incorporates two main components of climate risk: physical risk and transition risk.

Physical risk, initially considered as part of economic risk, is modeled further with a growing standard deviation that is accelerated yearly by a stochastic factor. This recognizes the uncertainty in climate response to greenhouse gas concentration. The CERM also incorporates the ability to drift the physical damage average intensity by a percentage of its standard deviation, acknowledging the possibility that rating agencies may only partially reflect the true magnitude of climate risk in their ratings. The equation used in the model also captures the auto-correlation characteristic of the chronic risks that arise from the geophysical inertia of climate change.

Transition risk represents the cost of the effort to mitigate carbon emission and to adapt to higher temperatures. The CERM models the transition effort as a loopback where the economy allocates resources in reaction to losses resulting from climate change. The model integrates our collective responsiveness to provide transition effort and its efficiency in slowing down climate change through available net-zero technologies. Additionally, the model incorporates a floor transition that reduces greenhouse gas emissions resulting from global economic recession in case of uncontrolled climate change.

To structure the lending portfolio, the CERM groups borrowers based on their credit ratings and sensitivities to climate risk of their business sector and geographic localisation. The CERM captures the sensitivity to climate risk factors of each group through micro-correlations, which are multiplicative to the macro physical and transition risk factors. These micro-correlations can be calculated based on data available on the market, considering greenhouse gas intensity for transition risk sensitivity and physical risk ratings from certain providers for physical damage sensitivity.

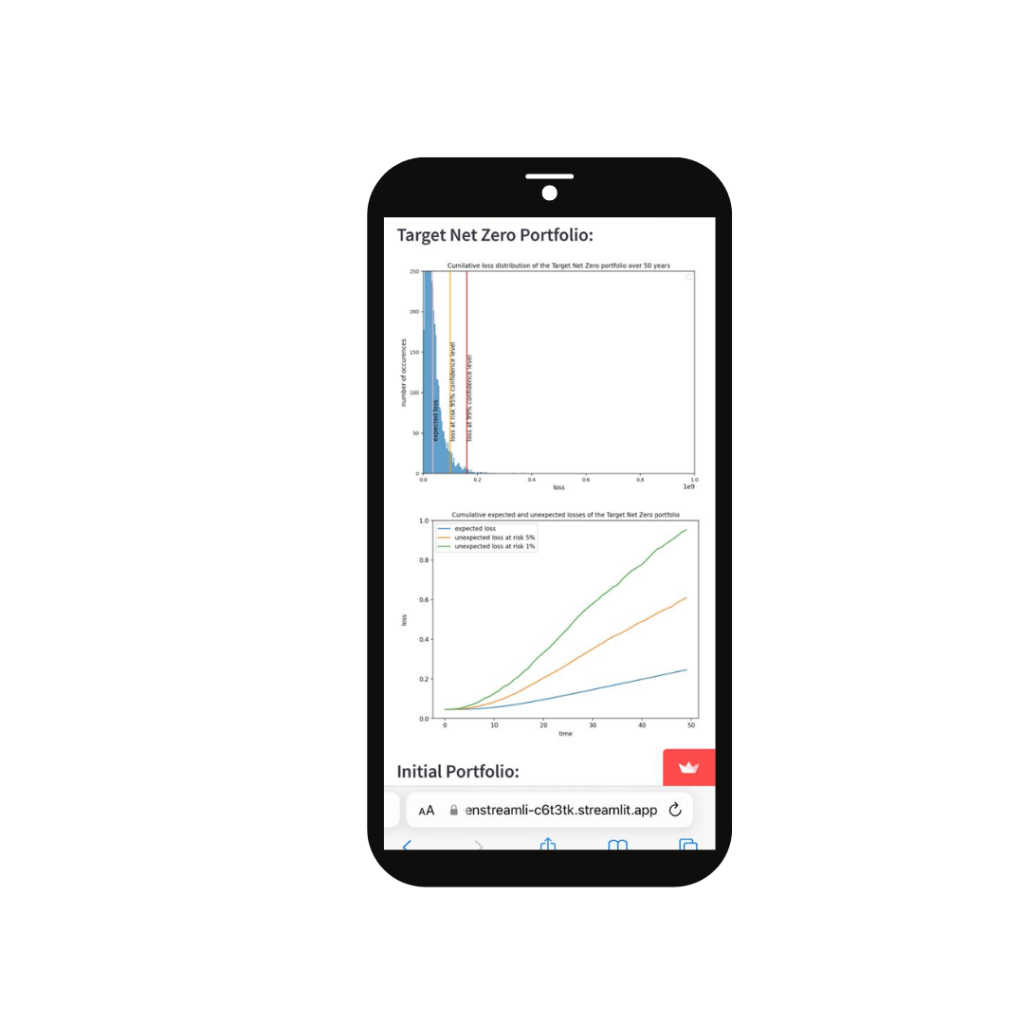

The CERM is a long-term, multi-step model that considers the evolution of the bank’s portfolio over several decades. It incorporates the changing micro-correlations of existing borrowers and the portfolio rebalancing strategy of the bank. An efficient net-zero transition positively impacts the credit loss distribution faced by the bank, serving as a way to mitigate climate risk alongside regulatory capital charges. However, the credibility of a bank’s net-zero strategy must be validated by the regulator. The positive dynamics of borrower sensitivities should align with the reality of transition investments funded by the bank. Credit ratings accessible during rebalancing should reflect the future financial health of economic sectors exposed to physical and transition risks.

By calculating the forward-looking distribution of the credit loss portfolio, including expected and unexpected losses, the CERM provides valuable insights for regulatory reporting and quantitative asset valuation. It enables banks to derive a loan and bond pricing mechanism, such as the “greenium,” that reflects the true risk mitigaion value of green investments. The CERM aligns with the goal of channeling capital toward the necessary net-zero transition while fulfilling the fiduciary obligations of banks towards their shareholders.